Key Highlights:

- A Digital Services Tax (DST) is a revenue-based tax on gross revenues from digital services, currently implemented by 15 countries

- Trump threatens new tariffs on countries with DSTs, claiming they discriminate against US tech giants while sparing Chinese firms

- The OECD’s framework requires countries to remove DSTs by 2024, though implementation remains incomplete

The Digital Services Tax has emerged as a major flashpoint in international trade relations, as President Donald Trump threatens to impose new tariffs on countries that levy these taxes on American technology companies. This revenue-based taxation mechanism, which targets multinational tech giants based on their local user activity rather than physical presence, represents a fundamental shift in how governments capture value from the digital economy. The growing tensions around the DST reflect deeper concerns about fair taxation in an increasingly digitized global economy, where traditional tax frameworks struggle to address the unique characteristics of digital business models.

Trump’s latest tariff threats specifically target nations implementing the Digital Services Tax, arguing that these measures unfairly discriminate against American companies like Google, Meta, and Amazon while providing exemptions for Chinese technology firms. The conflict highlights the complex intersection between taxation policy, trade relations, and the competitive landscape of global technology markets.

Understanding the Digital Services Tax Framework

- The Digital Services Tax operates as a revenue-based levy on gross income from digital activities, distinct from traditional profit-based corporate taxes

- Major tech companies face taxation based on user location rather than corporate headquarters or physical operations

The Digital Services Tax represents a fundamental departure from conventional corporate taxation models. Unlike traditional income taxes that focus on corporate profits, the Digital Services Tax applies to gross revenues generated from specific digital activities within a country’s jurisdiction. This approach enables governments to capture tax revenue from digital services provided to their citizens, regardless of whether the company maintains a physical presence in that territory.

The tax typically targets large multinational enterprises with significant digital operations and global revenues. Companies subject to the Digital Services Tax generally must meet specific revenue thresholds, with most countries setting minimum global revenue requirements of €750 million and local digital service revenues of €25 million annually. The Digital Services Tax covers various digital activities, including online advertising, digital marketplaces, social media platforms, search engines, and the sale or licensing of user data.

Countries implementing the Digital Services Tax argue that traditional tax frameworks fail to capture the value created through digital interactions with local users. The tax addresses situations where multinational tech companies generate substantial revenue from a country’s market without establishing sufficient taxable presence under existing international tax rules.

Global Implementation and Adoption Patterns

- Fifteen OECD countries have introduced or proposed Digital Services Tax measures, alongside several non-OECD nations

- Revenue generation from the Digital Services Tax reached over €400 million in France and the UK during 2021

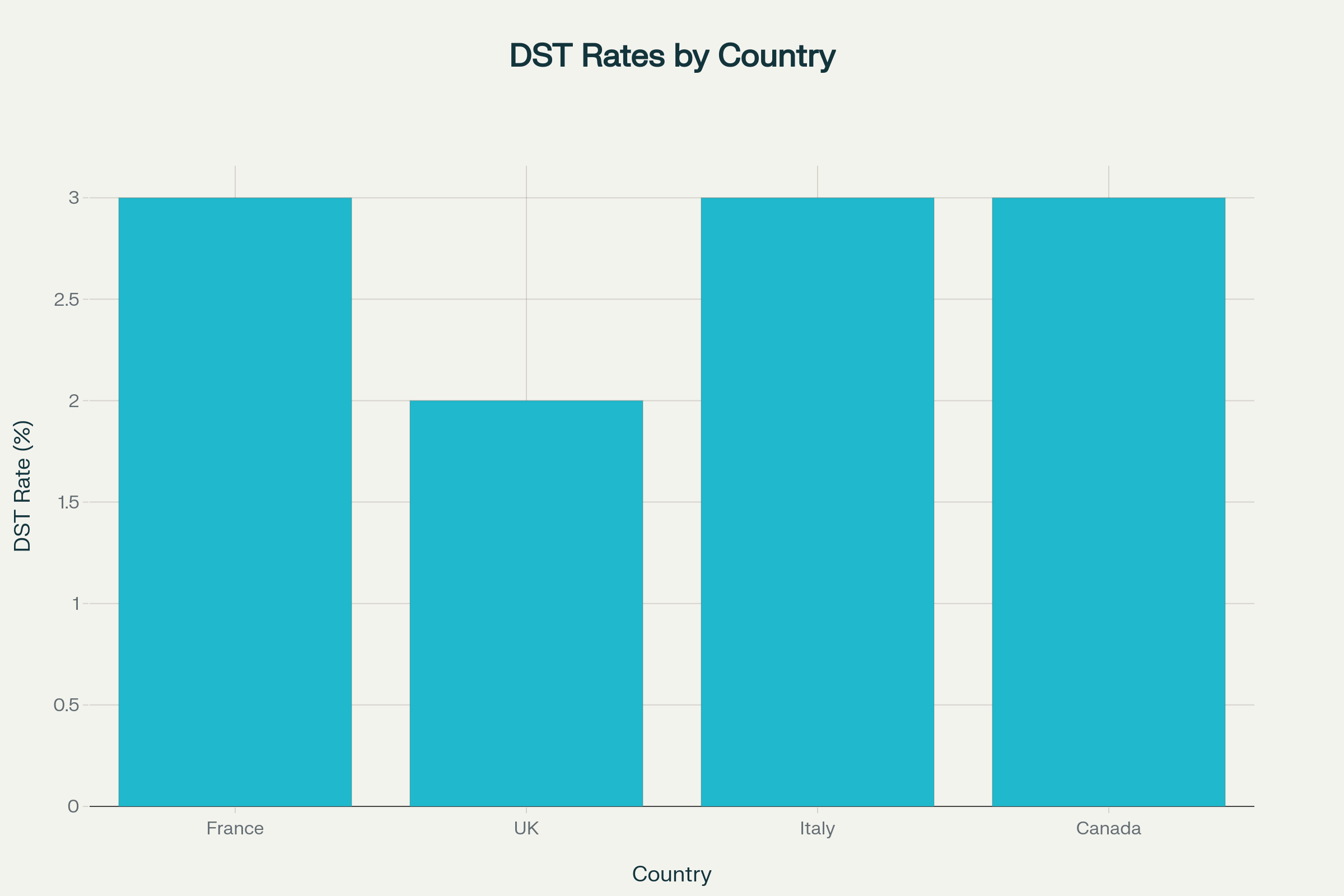

France pioneered the Digital Services Tax implementation in 2019, applying a 3% rate to revenues from digital interfaces, advertising, and user data. The United Kingdom followed in 2020 with a 2% Digital Services Tax on marketplaces, social media platforms, and search engines, generating significant revenue from major technology companies.

Italy implemented its Digital Services Tax in 2020 at a 3% rate, focusing on advertising and digital interface revenues. Canada joined the group more recently, introducing a 3% Digital Services Tax in June 2024, targeting digital services provided to Canadian users by companies meeting specific revenue thresholds.

Digital Services Tax implemented by various countries with rates, years, and scopes

European Union countries have been particularly active in Digital Services Tax adoption, with Austria, Spain, Turkey, and Hungary implementing various versions of the tax. Several countries including Belgium, Germany, and Poland have proposed or paused Digital Services Tax implementations pending international developments.

The revenue impact of the Digital Services Tax has proven substantial for implementing countries. France and the UK each generated over €400 million in Digital Services Tax revenue during 2021, demonstrating the significant financial implications for both governments and affected technology companies.

Trump’s Tariff Response and Strategic Concerns

- Trump views Digital Services Tax measures as discriminatory policies targeting American technology leadership while exempting Chinese competitors

- The threatened tariffs would restrict American chip exports to countries maintaining Digital Services Tax policies

President Trump’s opposition to the Digital Services Tax centers on claims that these measures discriminate against American technology companies while providing favorable treatment to Chinese firms. His administration argues that the Digital Services Tax unfairly targets major US corporations including Alphabet, Meta, and Amazon, potentially undermining America’s competitive position in global technology markets.

The proposed tariff response would specifically target countries maintaining DST policies, potentially restricting American semiconductor exports to those nations. This approach reflects Trump’s broader trade strategy of using economic leverage to pressure international partners on policies affecting US business interests.

Trump’s criticism extends beyond individual tax policies to encompass broader digital regulations, including Digital Services Legislation and Digital Markets Regulations. The administration characterizes these measures as systematic efforts to harm American technology companies while providing advantages to international competitors, particularly Chinese technology firms.

The tariff threats represent a significant escalation in trade tensions surrounding digital taxation, potentially affecting established trade relationships with key allies. Countries implementing the Digital Services Tax now face difficult choices between maintaining their tax policies and avoiding potential US trade retaliation.

International Framework and Future Developments

- The OECD‘s two-pillar solution requires countries to remove Digital Services Tax measures upon Pillar One implementation

- Current international agreements allow existing Digital Services Tax policies to continue until comprehensive global tax reforms take effect

The Organisation for Economic Co-operation and Development has developed a comprehensive framework addressing digital taxation challenges through its Base Erosion and Profit Shifting 2.0 project. This two-pillar approach aims to establish new international tax rules for the digital economy, with Pillar One specifically targeting the reallocation of taxing rights for large multinational enterprises.

Under the OECD framework, countries implementing the DST must remove these measures upon Pillar One implementation. However, the timeline for this transition remains uncertain, with implementation originally scheduled for 2024 but facing ongoing delays in international negotiations and domestic ratification processes.

The Unilateral Measures Compromise, agreed upon by the United States, United Kingdom, Spain, Austria, France, and Italy, allows member countries to maintain existing DST policies until Pillar One implementation. This agreement provides some stability for affected companies through tax credit mechanisms that offset Digital Services Tax payments against future tax liabilities.

Several countries have paused or delayed DST implementations pending OECD developments, including Canada, Brazil, and several European Union member states. These delays reflect ongoing uncertainty about the final structure of international digital tax reforms and their impact on existing national policies.

Final Assessment

The Digital Services Tax controversy illustrates the complex challenges of taxation in the digital age, where traditional territorial concepts of corporate presence no longer adequately capture economic value creation. Trump’s tariff threats represent a significant escalation in international trade tensions surrounding digital taxation, potentially affecting longstanding economic relationships with key allies. The outcome of these disputes will likely shape the future framework for international digital commerce and taxation.

While the OECD continues working toward comprehensive global solutions, the immediate tensions between DST policies and US trade threats create uncertainty for multinational technology companies operating across multiple jurisdictions. The resolution of these conflicts will require careful balancing of national tax sovereignty, fair international taxation principles, and the preservation of beneficial trade relationships in an increasingly interconnected digital economy.